The Pillar.

"They are watching the giant. He is watching the horizon. One factory, one customer, one horse — and something rising in the haze."

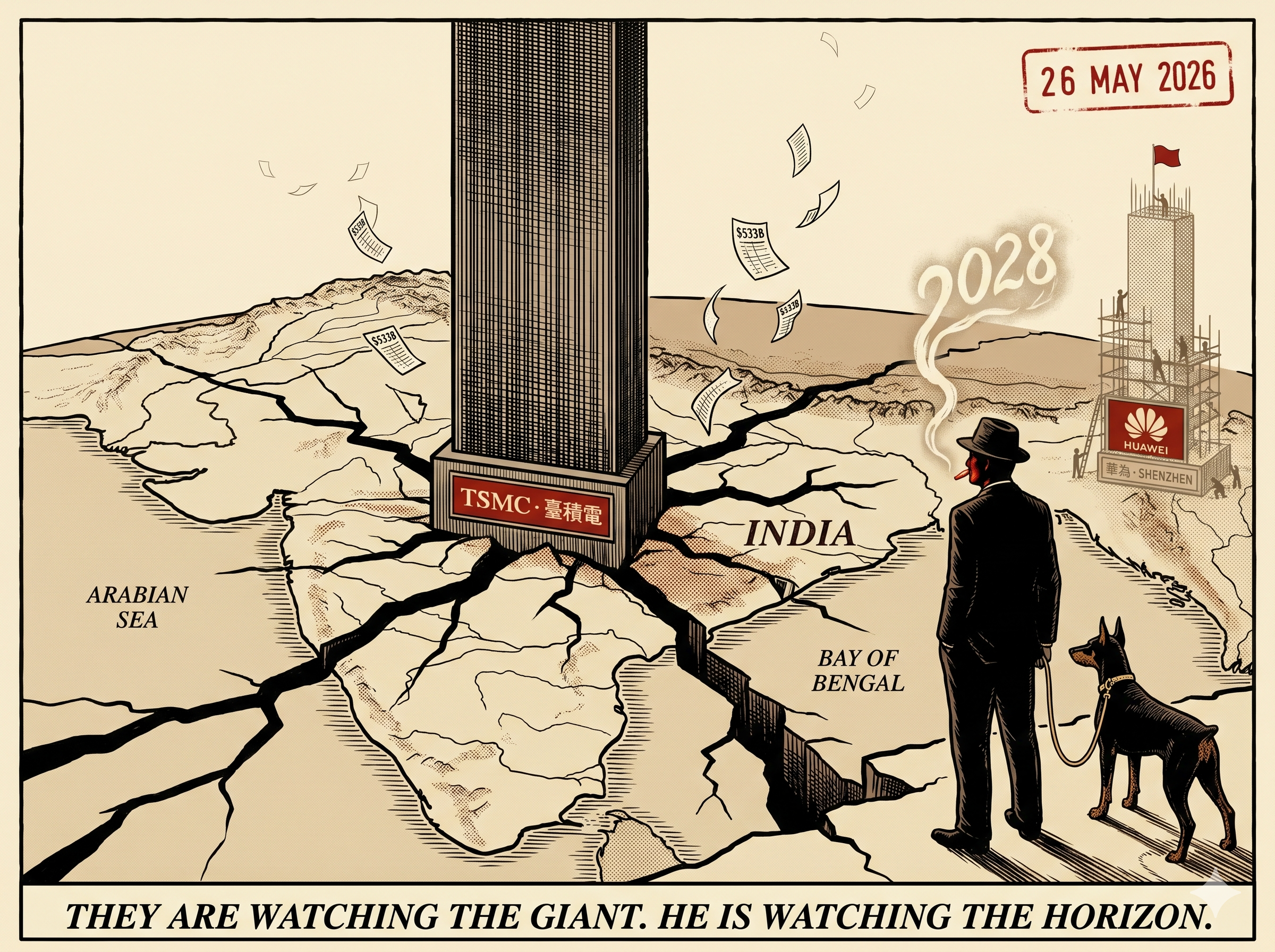

Bloomberg called it a milestone. Taiwan's stock market is now worth more than India's. The headline hides the math — almost half of Taiwan's entire market is one company. TSMC. The chip factory in a town called Hsinchu that makes the brains for Nvidia and Apple.

One factory. Worth more than every listed company in a country of 1.4 billion people. That isn't strength. That's everything riding on one horse. And on the eastern horizon — Adze sees a second pillar being built. Slow. Distant. Real.

"Taiwan beats India" is not the story.

India didn't lose to Taiwan. India lost $533 billion this year — its worst drop in fifteen years — and Taiwan kept grinding higher on the AI boom. The gap closed because one side fell, not because the other side won.

But look inside Taiwan's "market" and the picture gets uglier. TSMC alone is over 45% of the entire Taiwan index. Tech is nearly 80% of the whole market. So when you read "Taiwan beats India," what it really says is: one chip factory in Hsinchu, plus the suppliers feeding it, is now worth more than every listed company in a country of 1.4 billion people.

When the index is one name, it isn't a market. It's a single bet wearing a market's costume.

On the day the index hit a record, seven in ten stocks went down.

That's the tell. All the money is being sucked into TSMC and a handful of AI suppliers. Everyone else is starving.

If you owned the average Taiwanese stock, you'd think it was a bad year. If you owned the index, you'd think it was a great one. Same market. Two different realities. The gap between the headline and the ground truth — that's what late-cycle markets always look like, just before something cracks.

Reasonable on the surface. Terrifying underneath.

The number people quote — about 18 times what companies are expected to earn next year — sounds fine. But the bigger measure (total market value compared to the size of the actual economy) is past 440%. The classic danger line is 200%.

The only thing keeping it from being a clean bubble call: TSMC sells to Apple and Nvidia, not to Taiwanese shoppers. So comparing it to the local economy overstates things. Doesn't make it healthy. Just makes it less crazy than it looks on paper.

Everything rests on Nvidia. Nvidia rests on four names.

TSMC's biggest customer is Nvidia. Nvidia's biggest customers are four companies — Microsoft, Meta, Google, Amazon. If those four slow their AI spending even for a single quarter, TSMC's ability to charge premium prices weakens fast.

The market is acting like that can't happen. It can.

On the horizon, Huawei is building.

Huawei is rumoured to be closing the gap on TSMC's most advanced chips — and doing it without using American or European equipment. Not a 2026 problem. Probably a 2028 problem. But if they pull it off, TSMC's monopoly bonus goes away.

This is why Adze has his back to the giant. The pillar at the centre of the panel is what the world is staring at today. The half-built tower in the haze is what nobody is pricing yet. The cigarette ember is the focus. The smoke carries the date.

Three tells. Write them down now.

Your Dinasti fund is not a hedge.

You've been thinking of your Dinasti fund as a hedge against your China A-share fund. It isn't. They're both bets on the same thing — the global AI spending boom — just from different angles. If AI capex slows, they both fall together.

That's not diversification. That's two bets on the same horse with different jockeys.

Daily comic.

Long-reads when earned.

The daily noir runs every weekday at www.thelongend.com. Long-reads like this one — Field Reports — appear only when the daily comic has earned another permanent rule worth pulling out. Until next time: count the names before the index.

FIELD REPORT Nº 04 · CREDITS

- Series

- The Long End · Field Reports

- Report Nº

- FR-04

- Title

- The Pillar

- Date

- Mon 26 May 2026

- Format

- 1 Nano Banana panel + long-read body + Tape Gazette lesson card

- Cast

- Adze (watcher) · Twelve (Doberman) · Hiro Tanaka (filer of Lesson 004)

- Lesson

- Lesson 004 (FR) · "Count the names. Before the index." (Filed by Hiro.)

- Subject

- Taiwan's stock market overtaking India's. TSMC ~45% of Taiwan index. Tech ~80% of total market. Market-cap-to-GDP past 440%. 7-of-10 stocks down on record day. Huawei rising as the 2028 successor threat.

- Mythology seed

- 1987 clipping pinned under the new card — NTT (Nippon Telegraph & Telephone) alone worth more than the entire German stock market at peak, before the Tokyo bubble broke. The pattern is older than the corpus.

- Tells

- TSMC ADR breaks $354 (consensus crack) · TWSE breadth (index up, most stocks down) · US hyperscaler AI capex guidance flat/down.

- Arc state

- FR-04 logged; daily strip not advanced

- Imprint

- @ADZO · adezeno.com

- URL

- www.thelongend.com/field/fr-004

- ©

- 2026 The Long End · @ADZO · All rights reserved.